One-Asset HANK Tutorial#

The package supports heterogeneous agent models with and without porfolio chocie (i.e., with one asset and two assets, respectively). Start again with misc imports and load the package:

[1]:

import jax.numpy as jnp # use jax.numpy instead of normal numpy

from grgrlib import figurator, grplot # a nice backend for batch plotting with matplotlib

import econpizza as ep # pizza

import matplotlib.pyplot as plt

# only necessary if you run this in a jupyter notebook:

%matplotlib inline

We now look at the one-asset HANK, which is documented in the appendix of in the paper. The YAML file, with many comments, can be found in the examples folder.

Start with loading the example file:

[2]:

example_hank = ep.examples.hank

As before, example_hank is nothing else than the path to the YAML file:

[3]:

print(example_hank)

/home/gboehl/repos/econpizza/econpizza/examples/hank_with_comments.yml

Parse the example hank model from the yaml and compile the model:

[4]:

# parse model

hank1_dict = ep.parse(example_hank)

# compile the model

hank1 = ep.load(hank1_dict)

Creating grid variables:

...adding exogenous Rouwenhorst-grid for 'skills' with objects 'skills_grid', 'skills_transition' and 'skills_stationary'.

...adding endogenous log-grid for 'a' named 'a_grid'.

(load:) Parsing done.

The first step creates a raw dictionary from the yaml. The second translates everything to a model instance with compiled and tested functions. If something specific in your model does not work, you should have been informed by now.

Lets continue with the steady state:

[5]:

stst_result = hank1.solve_stst()

Iteration 1 | max. error 8.67e-01 | lapsed 0.9863

Iteration 2 | max. error 1.25e-01 | lapsed 1.1385

Iteration 3 | max. error 2.00e-03 | lapsed 1.2173

Iteration 4 | max. error 5.27e-07 | lapsed 1.2744

(solve_stst:) Steady state found (1.4549s). The solution converged.

By default, the final message is rather verbose. The rank of the Jacobian is important because quite often, the steady state is indetermined and some steady state values need to be fixed in advance. Econpizza can deal with that by using the Pseudoinverse during the Newton steps. Fixing some of the variables is also what I did here. Since the function has 12 degrees of freedom and 6 fixed variables for a total of 18 variables, we’re fine and the steady state solver nicely converges.

The resulting stst_result is similar to the return object from scipy.optimize.root and contains all sorts of nice information to help you debugging if you have problems finding the steady state:

[6]:

print(stst_result.keys())

dict_keys(['success', 'message', 'x', 'niter', 'fun', 'jac', 'aux', 'det', 'initial_values'])

[7]:

print(stst_result['fun']) # the steady state function at the solution x

[-2.70964118e-09 -5.68989300e-15 -1.07691633e-14 -1.11022302e-16

5.55111512e-17 0.00000000e+00 -2.22044605e-16 -1.11022302e-16

2.70963767e-09 0.00000000e+00 -2.74358133e-17 0.00000000e+00

0.00000000e+00 1.07078790e-11 1.11022302e-16 0.00000000e+00

0.00000000e+00 0.00000000e+00]

The pizza automatically stores the steady state values as a dictionary in the model object:

[8]:

hank1['stst']

[8]:

{'B': Array(5.6, dtype=float64),

'beta': Array(0.98, dtype=float64),

'C': Array(1., dtype=float64),

'div': Array(0.16666667, dtype=float64),

'mc': Array(0.83333333, dtype=float64),

'n': Array(0.94103603, dtype=float64),

'pi': Array(1., dtype=float64),

'R': Array(1.00395902, dtype=float64),

'Rn': Array(1.00395902, dtype=float64),

'Rr': Array(1.00395902, dtype=float64),

'Rstar': Array(1.00395902, dtype=float64),

'tax': Array(0.02217054, dtype=float64),

'Top10A': Array(0.3945656, dtype=float64),

'Top10C': Array(0.20142403, dtype=float64),

'w': Array(0.88554881, dtype=float64),

'y': Array(1., dtype=float64),

'y_prod': Array(1., dtype=float64),

'z': Array(1.06265857, dtype=float64)}

Let us, out of curiousity, have a look at the steady state distribution. It is stored under hank1['steady_state']. Note that at the same location, also steady state decisions (the value function) are stored.

[9]:

dist = hank1['steady_state']['distributions'][0]

grid = hank1['context']['a_grid']

hank1[context] is a dictionary that also stores some other model specific variables. Better have a look youself if you care. For those who really miss Dynare and the global access to model variables and objects, you can simply add the model context to globals:

[10]:

globals().update(hank1['context'])

print(a_grid) # this is now available while it was not before

[0.00000000e+00 2.85761999e-02 6.04187966e-02 9.59011550e-02

1.35439317e-01 1.79496881e-01 2.28590436e-01 2.83295620e-01

3.44253869e-01 4.12179939e-01 4.87870284e-01 5.72212399e-01

6.66195222e-01 7.70920734e-01 8.87616874e-01 1.01765194e+00

1.16255064e+00 1.32401196e+00 1.50392908e+00 1.70441160e+00

1.92781022e+00 2.17674438e+00 2.45413291e+00 2.76322829e+00

3.10765474e+00 3.49145079e+00 3.91911658e+00 4.39566661e+00

4.92668860e+00 5.51840896e+00 6.17776579e+00 6.91249027e+00

7.73119729e+00 8.64348644e+00 9.66005463e+00 1.07928214e+01

1.20550689e+01 1.34615974e+01 1.50288988e+01 1.67753502e+01

1.87214295e+01 2.08899549e+01 2.33063532e+01 2.59989575e+01

2.89993393e+01 3.23426792e+01 3.60681788e+01 4.02195210e+01

4.48453815e+01 5.00000000e+01]

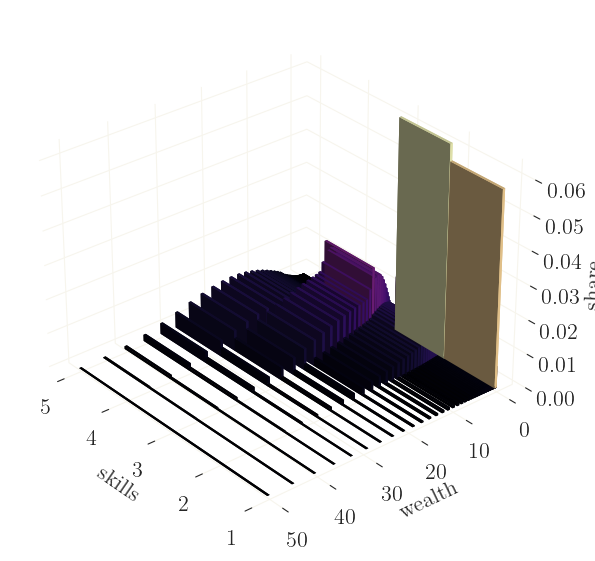

Let’s plot the distribution:

[11]:

from grgrlib import grbar3d # a nice backend to 3D-plots with matplotlib

ax, _ = grbar3d(dist, xedges=jnp.arange(1,5), yedges=grid, figsize=(9,7), depth=.5, zsort='max') # create 3D plot

# set axis labels

ax.set_xlabel('skills')

ax.set_ylabel('wealth')

ax.set_zlabel('share')

# rotate

ax.view_init(azim=140)

Nice. As expected, agents with higher income hold more assets, and vice versa. Note however that quantities are here given as shares of nodes on a log-grid (rather than true densities), meaning that shares for larger values on the grid are overrepresented.

Let’s continue with calculating some impulse response functions. We’ll have a look at a shock to the households’ discount factor \(\beta\).

Find the nonlinear IRFs (we will treat linear IRFs in the next tutorial):

[12]:

# define the shock as (shock_name, value)

shock = ('e_beta', 0.005)

# simulate

xst, flags = hank1.find_path(shock)

(get_derivatives:) Derivatives calculation done (4.085s).

(get_jacobian:) Jacobian accumulation and decomposition done (0.961s).

Iteration 1 | fev. 1 | error 7.96e-02 | inner 1.32e-08 | dampening 1.000

Iteration 2 | fev. 15 | error 4.06e-02 | inner 9.80e-06 | dampening 0.923

Iteration 3 | fev. 24 | error 9.98e-04 | inner 9.24e-06 | dampening 1.000

Iteration 4 | fev. 29 | error 4.45e-06 | inner 2.31e-07 | dampening 1.000

Iteration 5 | fev. 34 | error 1.69e-07 | inner 1.13e-08 | dampening 1.000

Iteration 6 | fev. 39 | error 7.82e-09 | inner 5.75e-10 | dampening 1.000 | lapsed 1.4236s

(find_path:) Stacking done (8.446s). The solution converged.

Alternatively, take the steady state as the initial value, and alter the initial value of \(\beta\) directly:

[13]:

# this is a dict containing the steady state values

x0 = hank1['stst'].copy()

# setting a large shock on the discount factor

x0['beta'] *= 1.009

# simulate again with the different initial state:

xst, flags = hank1.find_path(init_state=x0.values())

Iteration 1 | fev. 1 | error 1.29e-01 | inner 2.13e-08 | dampening 1.000

Iteration 2 | fev. 31 | error 8.30e-02 | inner 7.94e-02 | dampening 0.951

Iteration 3 | fev. 61 | error 1.20e-01 | inner 1.30e-04 | dampening 0.615

Iteration 4 | fev. 76 | error 5.87e-03 | inner 8.98e-06 | dampening 0.758

Iteration 5 | fev. 88 | error 2.95e-05 | inner 2.78e-06 | dampening 0.622

Iteration 6 | fev. 102 | error 2.52e-06 | inner 2.44e-07 | dampening 1.000

Iteration 7 | fev. 117 | error 2.21e-07 | inner 1.97e-08 | dampening 1.000

Iteration 8 | fev. 147 | error 2.61e-08 | inner 6.74e-09 | dampening 1.000

Iteration 9 | fev. 153 | error 4.75e-09 | inner 3.11e-10 | dampening 0.756 | lapsed 0.0023s

(find_path:) Stacking done (6.121s). The solution converged.

That went smoothly. Again, you will get (hopefully) meaningful and (hopefully) infomative final messages. Note that the second run was much faster than the first one. This is because the steady state sequence space Jacobian was already calculated and all functions were already compiled.

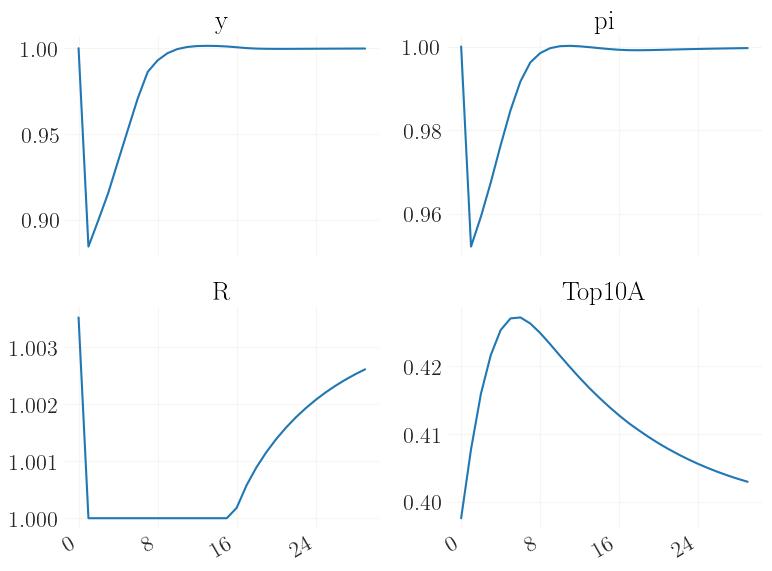

Let’s plot only a few of the variables for space restrictions: output \(y_t\) (Y), inflation \(\pi_t\) (pi), the nominal interst rate \(R_t\) (Rn), and the percentage share of wealth held by the top-10% richest, Top10A.

[14]:

# this is how *all* aggregate variables could be plotted:

#grplot(xst[:30], labels=hank1['variables'])

variables = 'y', 'pi', 'R', 'Top10A'

inds = [hank1['variables'].index(v) for v in variables] # get indices of variables

_ = grplot(xst[:30, inds], labels=variables)

See how the effective lower bound is binding for quite a while, and how the endogenous distribution adjusts accordingly.

In case you want to study the distributional dynamics in detail, you can also back out the exact nonlinear sequences of the disaggregated variables and their distribution. That is, their complete history given the trajectory xst of aggregated variables.

[15]:

# note that the sequence of aggregated variables is the input

het_vars = hank1.get_distributions(xst)

The function will return a dictionary with the disaggregated variables (outputs of the decision stage) and the distribution as key:

[16]:

print(het_vars.keys())

dict_keys(['WaPrime', 'a', 'c', 'dist'])

Each of the objects has shape *distribution shape, number_of_periods:

[17]:

print(het_vars['a'].shape)

(4, 50, 199)

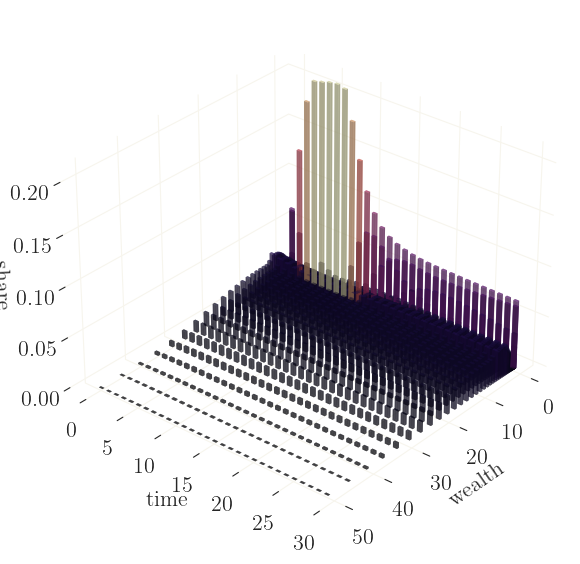

For example, we can use this to plot the distribution of wealth over time:

[18]:

dist = het_vars['dist']

a_grid = hank1['context']['a_grid']

# plot

ax, _ = grbar3d(dist[...,:30].sum(0), xedges=a_grid, yedges=jnp.arange(30), figsize=(9,7), depth=.5, width=.5, alpha=.5, zsort='max')

# set axis labels

ax.set_xlabel('wealth')

ax.set_ylabel('time')

ax.set_zlabel('share')

# rotate

ax.view_init(azim=50)

The graph shows that the discount factor shock (and the ZLB) mainly affects the wealth of the housholds which hold no or very few assets, giving incentive to hold more assets for a short period of time. Again, since these are shares of nodes on a log-grid (rather than true densities), the shares for larger values on the grid are overrepresented.